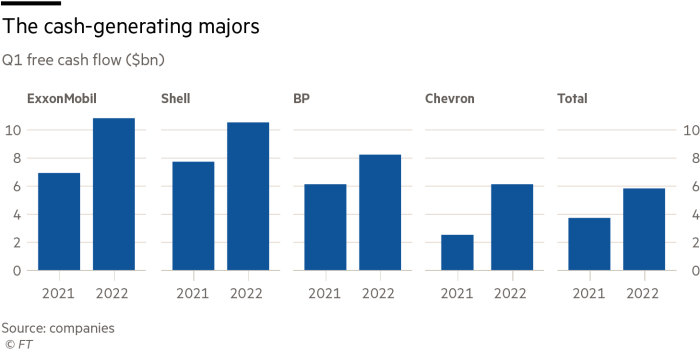

The world’s largest oil and gas companies are making more money than ever while spending relatively little.

European supermajors BP, Shell, and TotalEnergies have each pledged to become green companies over the next three decades but are still investing only a fraction of their capital in renewable energy.

With everyone expected to report another string of record earnings over the next week, bankers are wondering if they might be tempted to accelerate their transition strategies with a big acquisition.

Businesses haven’t stopped buying. In April, Shell acquired Indian energy group Sprng Energy from Actis for $1.55 billion; in May, Total acquired 50 percent of a US developer of wind and solar parks for $2.4 billion; and in June BP announced it had acquired a 40 percent stake in a huge Australian renewable energy project for an undisclosed sum.

Even US rival rafters — a relative laggard on climate commitments — spent $3.15 billion on the sustainable fuel-focused Renewable Energy Group in February.

But the deals are tiny compared to the tens of billions it would take to secure a transformative deal for a “green energy company” like RWE in Germany or Orsted in Denmark.

In the first year of the Covid-19 pandemic, when oil prices plummeted and the value of renewable energy companies soared, such a deal seemed all but impossible. In October 2020, Orsted’s market cap surpassed $70 billion, while Shell’s fell below $90 billion and BP’s to $51 billion, its lowest level since 1997.

This year, the rally in oil and gas prices has helped Shell’s shares soar 30 percent, taking the valuation back above $185 billion. By contrast, Orsted’s market cap has fallen to $46 billion and its shares are down about 3 percent since January.

However, Jim Peterkin, head of oil and gas at investment bank Credit Suisse, said the time for such deals was coming but still a long way off.

“I think there will be consolidation over time, but that may be 10 years away, not a year,” he said.

Despite the shift in relative valuations, increased investor support for companies more focused on renewable energy meant companies like Orsted and RWE continued to trade at much higher prices than legacy oil and gas majors, Peterkin added.

“The multiples haven’t changed,” he said, so large-scale acquisitions of renewable energy companies are “still dilutive.”

Shell CEO Ben van Beurden told the Financial Times he has held back on big deals to give Shell more time to better understand the renewable energy sector.

“At some point, I would expect there to be a time for large, inorganic ones [growth], but you don’t want to start if you’re a relative newbie on the block,” he said. “We’ve looked at a lot of big things before that that didn’t work out or that we didn’t decide to do . . . and today I congratulate myself that I didn’t.”

If Shell would make a big move, he added the number of electricity customers The target company would be more important than the number of power assets.

Others in the industry point to a lack of viable targets for a blockbuster acquisition.

“Yes, it makes sense, but there’s no obvious deal,” said a senior investment banker. “There aren’t many goals that are truly transformative, and the bigger ones, like RWE or Orsted, aren’t really actionable.”

Orsted is majority-owned by the Danish government, the banker added successful acquisitions of listed German companies like RWE are rare.

Total has been the most active of the supermajors in flashy deals. According to Bernstein analysts, the French group made about $6 billion in low-carbon investments between 2010 and 2020, as much as BP and Shell combined. Investment bank RBC Capital Markets values Total’s low-carbon business at $35 billion, compared to $24 billion for Shell and just $12 billion for BP.

Bankers say Total has been more willing than its peers to partner with renewable energy companies rather than make outright acquisitions. Last year it bought 20 percent Participation in Adani Green Energy for $2.5 billion at a discount of nearly 40 percent to the Indian group’s market capitalization.

In May Total acquired 50 percent of the US company Clearway Energy Group from Global Infrastructure Partners. As Clearway owns 42 percent of its publicly traded subsidiary Clearway Energy Inc, the transaction gives Total access to a 25-gigawatt pipeline of wind, solar, and storage projects in the United States.

Total limited the amount of cash it had to pay to $1.6 billion by investing in the parent company rather than the public company and selling GIP a stake in its SunPower business in the same transaction.

“This is what smart M&A looks like to me for an energy major of the future,” said Peterkin.

Total boss Patrick Pouyanné, who tends to avoid bankers and prefers to deal directly with deals like the one with Clearway, told the FT that the challenge for the old oil and gas companies is to make renewable energy sufficiently profitable.

“Our DNA is that we love the volatility of gasoline and gas commodities. . . We know there can be lows, but there can also be highs,” he said. “It’s not a utility, it’s people who accept a regulated and controlled level of return.”

As a result, companies like Total must acquire or develop renewable energy companies where at least some of the electricity generated is not subject to regulated tariffs. “For example, if I have 70 percent of my park under regulated tariffs and have 30 to 40 percent of production outside of that, I can make a lot of money,” Pouyanné said.

For now, the supermajors have yet to show if they can run renewable energy companies profitably — let alone, in terms of successful mergers and acquisitions, more profitably than their current owners.

To agree to a deal, shareholders in an oil and gas company would have to be convinced it could run a company like RWE’s assets better than they currently do, said the head of a renewable energy-focused private equity group.

Many industry insiders remain skeptical about oil and gas companies’ ability to take the plunge.

One suggestion is that by bringing their trading expertise to the electricity market, European supermajors could increase returns on the renewable energy projects they manage.

The trading expertise of BP, Shell, and Total stands out, even in the oil industry, and all three have built large electricity trading companies. Access to Total’s power trading capabilities was offered as part of the recent Clearway deal.

If European supermajors can leverage this advantage to earn “double-digit returns” from developing and owning renewable energy assets, it would go a long way in convincing shareholders to support a major acquisition in the future, said Peterkin.

Until then, most in the industry expect the largest deals to remain in the $1 billion to $5 billion range, meaning billions of dollars per quarter will continue to flow back to shareholders in the form of buybacks and dividends.

Shell has already made $8.5 billion in share buybacks this year, and van Beurden said shareholders should expect more.